DeFi

Jan 1, 2025

DeFi

DeFi

Photo by: gstudioimagen on FreePik

Web3 technology has led to breakthrough transformations for many industries, particularly for finance with its long-established systems and bureaucracy. Blockchain's transparent, decentralized ledger system reduces intermediary dependencies, making transactions faster, more secure and less cost-consuming. This shift towards decentralized finance (DeFi) has been amplified with developments in permissionless, peer-to-peer platforms for how people and institutions access financial services. Web3 empowers smart contracts to support automated execution and allows tokenized investments in previously inaccessible assets restricted by location or wealth requirements. In this article, we will learn how the blockchain is disrupting the financial sector and discuss the increasing popularity of DeFi vs TradFi and the host of opportunities and obstacles that await.

Blockchain is a secure, decentralized digital ledger. Unlike the conventional financial system that relies on centralized entities like banks, the Federal Reserve, and clearinghouses to validate and process transactions, blockchains operate through a decentralized network of nodes. These nodes validate transactions using consensus mechanisms like Proof of Work or Proof of Stake, eliminating the need for centralized processing or entities. This model makes activity transparent, immutable, and resistant to unauthorized alterations making it fit for finance, supply chain, healthcare and more. It forms the backbone of DeFi protocols and holds the potential to revolutionize the financial world.

This innovation has given rise to digital currencies, tokenization of assets, and robust peer-to-peer payment platforms. By streamlining processes, blockchain reduces inefficiencies, minimizes costs, and accelerates transaction speeds. Traditional financial systems, with their multi-layered infrastructures and manual reconciliations, often face delays and high operational expenses compared to a decentralized money system. Blockchain addresses these challenges by embedding trust directly into its framework, confirming transactions are secure and tamper-proof.

The result is more accessible, efficient, and user-empowered financial institutions. Blockchain not only enhances productivity but also challenges conventional financial practices, paving the way for a future where technology drives transparency and cost-effectiveness in finance. The idea of central bank digital currency (CBDC) is emerging as a potential advancement that would mark one of the biggest changes in financial systems in decades. The Federal Reserve and other central banks are investigating CBDCs to potentially integrate TradFi with DeFi for improved financial accessibility and efficiency.

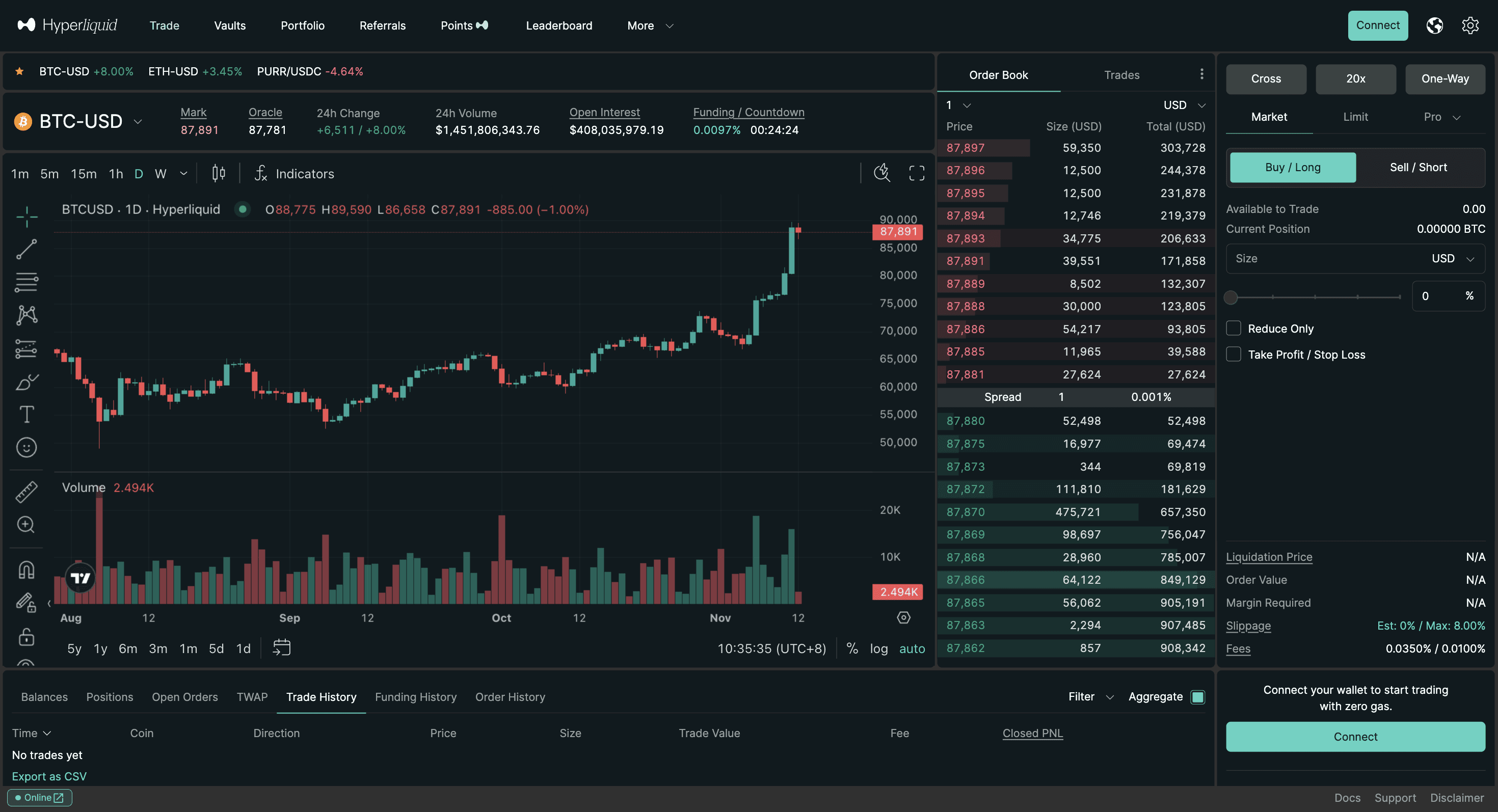

Decentralized finance (DeFi) is one of the most disruptive technologies of blockchain as it eliminates the need for traditional financial establishments. DeFi trading platforms allow traders to borrow, lend, and trade without an intermediary, but on smart contracts, which are programs that automatically execute on the blockchain.

On the other hand, TradFi includes traditional banking and institutionalized stock markets. Even though these establishments have been pillars of global economies for hundreds of years, they often receive backlash due to their exclusive nature.

Comparing DeFi vs TradFi reveals some key differences:

Access and Financial Inclusion: Anyone with internet access is able to use DeFi platforms, while TradFi often requires wealth minimums and specific locations, leading to unbanked and under-banked populations

Transparency: Blockchain systems are all record and maintain on distributed ledgers and therefore can easily be verified. In contrast, in TradFi, much is kept in the black box of a centralized entities private systems.

Costs: Through the use of DeFi, various services can be obtained at lower costs due to the absence of centralized intermediaries but in TradFi, hefty fees accompany banking services and asset management.

Centralized finance (CeFi) serves as a bridge between traditional financial systems and DeFi. CeFi relies on traditional financial theories while integrating cryptocurrencies, acting as an intermediary that offers users familiar services akin to banks. This facilitates financial transactions in both fiat and digital currencies, like PayPal combining cash and PYUSD in one wallet.

The tokenization of Real World Assets (RWA) is one of the most transformative use cases for blockchain innovations in the financial industry. RWA Tokenization converts tangible assets (such as real estate, precious metals, commodities and fine art) into a digital token asset on-chain. These digital assets can be traded, in lieu of the real asset, safely and easily into the financial ecosystem. Unlike normal ownership models, tokenized assets can be fractionalized to allow a much larger audience to buy in. These innovations are rapidly changing how we engage with traditional finance.

In the past, illiquid assets, such as real estate and luxury goods, were bought and sold with large currency and long periods of time. These assets are tokenized, which means they are divided into smaller units or tokens, such that investors can purchase fractional ownership. With the click of a button, investors can now easily acquire fractional ownership of high-value assets, such as luxury apartments, adding an entirely new level of liquidity in traditionally static markets.

Tokenization makes high-value asset investment less cumbersome. Traditionally, investing in premium real estate or art is prohibitively capital-heavy, restricting the asset class to rich individuals and institutions. With tokenization, anyone with a budget (modest) can now buy fractions of these digital assets, opening the way towards even greater participation in lucrative markets. The democratization of finance allows more people to participate and more people out of the economic system. And it closes the gap between individual investors and elite opportunities.

The basis for tokenization is blockchain technology, which offers a distributed ledger system that is immutable and secure. Ownership of assets can be accessed in real time so that there are no grey areas or conflicts. Also, the tokenized transactions do not require intermediaries, thereby lessening time, complications, and expenses associated with the traditional centralized exchanges. Further, the integration of blockchain into the transaction processes also increases the level of trust among investors since the provision of transaction history is complete and unchangeable.

Consider RWA tokenization in real estate. Companies no longer need brokers to divide the ownership of real estate. The art market was also transformed since artists could offer any fraction of their collections to the global market. The trading of commodities has also improved, enabling investors to conveniently purchase tokenized gold or oil.

All these mean that RWA tokenization is widening the opportunities in the financial market, and when coupled with the ease of trading cryptocurrencies, it will create an efficient ecosystem and new possibilities for investors. This comes as an encouragement for future investments and the promise of more effective mechanisms for the mobilization of capital.

Peer-to-peer payments enable money to move globally in a more streamlined manner; regardless of traditional intermediaries such as banks or payment processors, a user is able to move money to another directly using cryptocurrencies or stablecoins. In contrast, centralized exchanges act as intermediaries in Centralized Finance (CeFi), supporting both fiat and digital currencies.

This is a game changer for financial inclusion, especially in regions that are underserved or completely unbanked. Usually, this form of finance excludes millions due to geographical, infrastructural, or economic causes. Decentralized solutions seem to be the answer as they facilitate quick and inexpensive payments directly connecting the parties on a global scale.

Fintech, which refers to financial technology, is yet another way of disrupting the traditional financial systems, along with offering mobile banking and lending online, as well as digital wallets. With the help of blockchain technology, Fintech companies are able to broaden their scope of services through:

Decentralized Applications (dApps): Blockchain-based platforms relying on DeFi protocols create the possibility of providing services like lending, borrowing, and insurance with less dependence on third parties.

Digital Identity Solutions: Identity verification on the basis of blockchain guarantees security and ease of mounting customer registration on Fintech platforms.

Tokenized Financial Instruments: Another area of innovation is tokenization — made possible by blockchain — that makes by-Fintech firms appear more attractive to many investors by allowing the creation of entirely new investment products.

The integration of decentralized finance and Fintech has induced transformational creative growth never seen before, which calls for a future where services relevant to finance will be rendered in an efficient time period, cut across social gaps, providing equitable services for all. This future realizes a comprehensive financial ecosystem that allies traditional finance (TradFi) with decentralized finance (DeFi), boosting financial services accessibility, regulatory compliance, and consumer protection.

DeFi trading platforms are revolutionizing the finance industry as the central feature of blockchain. Users can trade cryptocurrencies, lending assets, or earn interest on liquidity pools – all within a transparent financial system that reduces risks from traditional parties.

DeFi trading platforms implement smart contracts, resulting in high levels of transactional certainty, reducing but not eliminating the likelihood of human errors or fraud, which differs greatly from deposits in the traditional finance systems.

As more of these platforms come into view, it begins to suggest there is a tendency for a more user-oriented structure of the financial industry, where a greater degree of control and involvement is expected. Nevertheless, these platforms are still subject to parameters of security and regulations to enhance their acceptance as mainstream methods compared to centralized financial services.

DeFi is not without its troubles, some of which include regulation, security, and scalability. Slow, central banks and the Federal Reserve still play a crucial role in stabilizing global financial systems and have responded to blockchain innovations with cautious interest, recognizing both its potential and the challenges it presents. Primary hurdles when it comes to use over traditional finance:

Regulatory Uncertainty: At the moment, governments and other authorities all over the globe are still trying to figure out the categorization and regulation of assets and systems based on blockchain technology. For instance, the U.S. SEC has been actively categorizing tokens as securities, sparking debates within the industry.

Scalability: For widespread usage and the ability to carry out numerous transactions, blockchain networks have to solve the scalability problem.

Security Concerns: Even if, in general, a blockchain is secure, exploits can occur owing to some vulnerabilities in the smart contracts or poor platform design. Unfamiliarity with the technology makes this concern even greater.

Integration with Legacy Systems: Introducing blockchain technology into the existing financial landscape is a challenge which necessitates investment and cooperation.

Oppositely though, the opportunities provided are as equally compelling. Further, blockchain enables:

Global Financial Inclusion: DeFi ensures adequate financial services reach the unbanked and under-banked populations.

Enhanced Transparency: Since it is impossible to alter or delete blockchain records, such technology guarantees reliability and responsibility when carrying out transactions.

Innovative Financial Products: Tokenized real estate, decentralized insurance, and other products illustrate how blockchain spurs imagination in developing financial stability.

It appears inevitable that the mixing of TradFi and DeFi will result in a hybrid financial system combining the best of both worlds. The traditional financial institutions are testing the use of blockchain technology to improve their offerings, while the DeFi ecosystem is coming up with ways to adhere to regulatory requirements and tackle scale issues.

This convergence, however, could make blockchain innovations such as RWA tokenization, peer–to–peer payments and decentralized lending seamlessly integrated into traditional finance and asset management.

The global financial crisis, such as the 2008 collapse of Lehman Brothers, significantly impacted the financial landscape and led to subsequent reforms aimed at preventing future crises. The decentralization, transparency, and efficiency of blockchain can overcome many inefficiencies of TradFi, thus making decentralized finance a serious competitor in redefining the financial industry. RWA tokenization, DeFi trading platforms and P2P payment solutions are already showing promise by creating faster, cheaper and more financially inclusive alternatives to the traditional systems. But TradFi is thoroughly embedded in the global economy supported by its regulatory frameworks, trusted institutions, and decades of infrastructural experience.

Instead, a hybrid model is probably what we can expect in the future whereby blockchain is supplemented by conventional finance. However, according to the report, the use of blockchain by TradFi institutions for settlement processes, digital asset management, and tokenization of financial instruments is becoming more common. At the same time, DeFi platforms are looking to overcome issues such as scalability and regulatory compliance to extend it to a broader mass audience. Herein lays the potential for this synergy to create a financial ecosystem in which blockchain facilitates TradFi with greater efficiency and inclusivity rather than displacing it wholesale.

Traditional finance is getting a makeover thanks to decentralization, which bolsters transparency, efficiency, and inclusivity. DeFi trading platforms, RWA tokenization and peer-to-peer payments aren't just challenging the status quo but creating a fairer, more open financial system. It’s only a matter of time until the DeFi and TradFi worlds collide, and the way the two interact will determine a future where financial services are truly democratized, pioneering, and agile.

Web3 technology has led to breakthrough transformations for many industries, particularly for finance with its long-established systems and bureaucracy. Blockchain's transparent, decentralized ledger system reduces intermediary dependencies, making transactions faster, more secure and less cost-consuming. This shift towards decentralized finance (DeFi) has been amplified with developments in permissionless, peer-to-peer platforms for how people and institutions access financial services. Web3 empowers smart contracts to support automated execution and allows tokenized investments in previously inaccessible assets restricted by location or wealth requirements. In this article, we will learn how the blockchain is disrupting the financial sector and discuss the increasing popularity of DeFi vs TradFi and the host of opportunities and obstacles that await.

Blockchain is a secure, decentralized digital ledger. Unlike the conventional financial system that relies on centralized entities like banks, the Federal Reserve, and clearinghouses to validate and process transactions, blockchains operate through a decentralized network of nodes. These nodes validate transactions using consensus mechanisms like Proof of Work or Proof of Stake, eliminating the need for centralized processing or entities. This model makes activity transparent, immutable, and resistant to unauthorized alterations making it fit for finance, supply chain, healthcare and more. It forms the backbone of DeFi protocols and holds the potential to revolutionize the financial world.

This innovation has given rise to digital currencies, tokenization of assets, and robust peer-to-peer payment platforms. By streamlining processes, blockchain reduces inefficiencies, minimizes costs, and accelerates transaction speeds. Traditional financial systems, with their multi-layered infrastructures and manual reconciliations, often face delays and high operational expenses compared to a decentralized money system. Blockchain addresses these challenges by embedding trust directly into its framework, confirming transactions are secure and tamper-proof.

The result is more accessible, efficient, and user-empowered financial institutions. Blockchain not only enhances productivity but also challenges conventional financial practices, paving the way for a future where technology drives transparency and cost-effectiveness in finance. The idea of central bank digital currency (CBDC) is emerging as a potential advancement that would mark one of the biggest changes in financial systems in decades. The Federal Reserve and other central banks are investigating CBDCs to potentially integrate TradFi with DeFi for improved financial accessibility and efficiency.

Decentralized finance (DeFi) is one of the most disruptive technologies of blockchain as it eliminates the need for traditional financial establishments. DeFi trading platforms allow traders to borrow, lend, and trade without an intermediary, but on smart contracts, which are programs that automatically execute on the blockchain.

On the other hand, TradFi includes traditional banking and institutionalized stock markets. Even though these establishments have been pillars of global economies for hundreds of years, they often receive backlash due to their exclusive nature.

Comparing DeFi vs TradFi reveals some key differences:

Access and Financial Inclusion: Anyone with internet access is able to use DeFi platforms, while TradFi often requires wealth minimums and specific locations, leading to unbanked and under-banked populations

Transparency: Blockchain systems are all record and maintain on distributed ledgers and therefore can easily be verified. In contrast, in TradFi, much is kept in the black box of a centralized entities private systems.

Costs: Through the use of DeFi, various services can be obtained at lower costs due to the absence of centralized intermediaries but in TradFi, hefty fees accompany banking services and asset management.

Centralized finance (CeFi) serves as a bridge between traditional financial systems and DeFi. CeFi relies on traditional financial theories while integrating cryptocurrencies, acting as an intermediary that offers users familiar services akin to banks. This facilitates financial transactions in both fiat and digital currencies, like PayPal combining cash and PYUSD in one wallet.

The tokenization of Real World Assets (RWA) is one of the most transformative use cases for blockchain innovations in the financial industry. RWA Tokenization converts tangible assets (such as real estate, precious metals, commodities and fine art) into a digital token asset on-chain. These digital assets can be traded, in lieu of the real asset, safely and easily into the financial ecosystem. Unlike normal ownership models, tokenized assets can be fractionalized to allow a much larger audience to buy in. These innovations are rapidly changing how we engage with traditional finance.

In the past, illiquid assets, such as real estate and luxury goods, were bought and sold with large currency and long periods of time. These assets are tokenized, which means they are divided into smaller units or tokens, such that investors can purchase fractional ownership. With the click of a button, investors can now easily acquire fractional ownership of high-value assets, such as luxury apartments, adding an entirely new level of liquidity in traditionally static markets.

Tokenization makes high-value asset investment less cumbersome. Traditionally, investing in premium real estate or art is prohibitively capital-heavy, restricting the asset class to rich individuals and institutions. With tokenization, anyone with a budget (modest) can now buy fractions of these digital assets, opening the way towards even greater participation in lucrative markets. The democratization of finance allows more people to participate and more people out of the economic system. And it closes the gap between individual investors and elite opportunities.

The basis for tokenization is blockchain technology, which offers a distributed ledger system that is immutable and secure. Ownership of assets can be accessed in real time so that there are no grey areas or conflicts. Also, the tokenized transactions do not require intermediaries, thereby lessening time, complications, and expenses associated with the traditional centralized exchanges. Further, the integration of blockchain into the transaction processes also increases the level of trust among investors since the provision of transaction history is complete and unchangeable.

Consider RWA tokenization in real estate. Companies no longer need brokers to divide the ownership of real estate. The art market was also transformed since artists could offer any fraction of their collections to the global market. The trading of commodities has also improved, enabling investors to conveniently purchase tokenized gold or oil.

All these mean that RWA tokenization is widening the opportunities in the financial market, and when coupled with the ease of trading cryptocurrencies, it will create an efficient ecosystem and new possibilities for investors. This comes as an encouragement for future investments and the promise of more effective mechanisms for the mobilization of capital.

Peer-to-peer payments enable money to move globally in a more streamlined manner; regardless of traditional intermediaries such as banks or payment processors, a user is able to move money to another directly using cryptocurrencies or stablecoins. In contrast, centralized exchanges act as intermediaries in Centralized Finance (CeFi), supporting both fiat and digital currencies.

This is a game changer for financial inclusion, especially in regions that are underserved or completely unbanked. Usually, this form of finance excludes millions due to geographical, infrastructural, or economic causes. Decentralized solutions seem to be the answer as they facilitate quick and inexpensive payments directly connecting the parties on a global scale.

Fintech, which refers to financial technology, is yet another way of disrupting the traditional financial systems, along with offering mobile banking and lending online, as well as digital wallets. With the help of blockchain technology, Fintech companies are able to broaden their scope of services through:

Decentralized Applications (dApps): Blockchain-based platforms relying on DeFi protocols create the possibility of providing services like lending, borrowing, and insurance with less dependence on third parties.

Digital Identity Solutions: Identity verification on the basis of blockchain guarantees security and ease of mounting customer registration on Fintech platforms.

Tokenized Financial Instruments: Another area of innovation is tokenization — made possible by blockchain — that makes by-Fintech firms appear more attractive to many investors by allowing the creation of entirely new investment products.

The integration of decentralized finance and Fintech has induced transformational creative growth never seen before, which calls for a future where services relevant to finance will be rendered in an efficient time period, cut across social gaps, providing equitable services for all. This future realizes a comprehensive financial ecosystem that allies traditional finance (TradFi) with decentralized finance (DeFi), boosting financial services accessibility, regulatory compliance, and consumer protection.

DeFi trading platforms are revolutionizing the finance industry as the central feature of blockchain. Users can trade cryptocurrencies, lending assets, or earn interest on liquidity pools – all within a transparent financial system that reduces risks from traditional parties.

DeFi trading platforms implement smart contracts, resulting in high levels of transactional certainty, reducing but not eliminating the likelihood of human errors or fraud, which differs greatly from deposits in the traditional finance systems.

As more of these platforms come into view, it begins to suggest there is a tendency for a more user-oriented structure of the financial industry, where a greater degree of control and involvement is expected. Nevertheless, these platforms are still subject to parameters of security and regulations to enhance their acceptance as mainstream methods compared to centralized financial services.

DeFi is not without its troubles, some of which include regulation, security, and scalability. Slow, central banks and the Federal Reserve still play a crucial role in stabilizing global financial systems and have responded to blockchain innovations with cautious interest, recognizing both its potential and the challenges it presents. Primary hurdles when it comes to use over traditional finance:

Regulatory Uncertainty: At the moment, governments and other authorities all over the globe are still trying to figure out the categorization and regulation of assets and systems based on blockchain technology. For instance, the U.S. SEC has been actively categorizing tokens as securities, sparking debates within the industry.

Scalability: For widespread usage and the ability to carry out numerous transactions, blockchain networks have to solve the scalability problem.

Security Concerns: Even if, in general, a blockchain is secure, exploits can occur owing to some vulnerabilities in the smart contracts or poor platform design. Unfamiliarity with the technology makes this concern even greater.

Integration with Legacy Systems: Introducing blockchain technology into the existing financial landscape is a challenge which necessitates investment and cooperation.

Oppositely though, the opportunities provided are as equally compelling. Further, blockchain enables:

Global Financial Inclusion: DeFi ensures adequate financial services reach the unbanked and under-banked populations.

Enhanced Transparency: Since it is impossible to alter or delete blockchain records, such technology guarantees reliability and responsibility when carrying out transactions.

Innovative Financial Products: Tokenized real estate, decentralized insurance, and other products illustrate how blockchain spurs imagination in developing financial stability.

It appears inevitable that the mixing of TradFi and DeFi will result in a hybrid financial system combining the best of both worlds. The traditional financial institutions are testing the use of blockchain technology to improve their offerings, while the DeFi ecosystem is coming up with ways to adhere to regulatory requirements and tackle scale issues.

This convergence, however, could make blockchain innovations such as RWA tokenization, peer–to–peer payments and decentralized lending seamlessly integrated into traditional finance and asset management.

The global financial crisis, such as the 2008 collapse of Lehman Brothers, significantly impacted the financial landscape and led to subsequent reforms aimed at preventing future crises. The decentralization, transparency, and efficiency of blockchain can overcome many inefficiencies of TradFi, thus making decentralized finance a serious competitor in redefining the financial industry. RWA tokenization, DeFi trading platforms and P2P payment solutions are already showing promise by creating faster, cheaper and more financially inclusive alternatives to the traditional systems. But TradFi is thoroughly embedded in the global economy supported by its regulatory frameworks, trusted institutions, and decades of infrastructural experience.

Instead, a hybrid model is probably what we can expect in the future whereby blockchain is supplemented by conventional finance. However, according to the report, the use of blockchain by TradFi institutions for settlement processes, digital asset management, and tokenization of financial instruments is becoming more common. At the same time, DeFi platforms are looking to overcome issues such as scalability and regulatory compliance to extend it to a broader mass audience. Herein lays the potential for this synergy to create a financial ecosystem in which blockchain facilitates TradFi with greater efficiency and inclusivity rather than displacing it wholesale.

Traditional finance is getting a makeover thanks to decentralization, which bolsters transparency, efficiency, and inclusivity. DeFi trading platforms, RWA tokenization and peer-to-peer payments aren't just challenging the status quo but creating a fairer, more open financial system. It’s only a matter of time until the DeFi and TradFi worlds collide, and the way the two interact will determine a future where financial services are truly democratized, pioneering, and agile.

Web3 technology has led to breakthrough transformations for many industries, particularly for finance with its long-established systems and bureaucracy. Blockchain's transparent, decentralized ledger system reduces intermediary dependencies, making transactions faster, more secure and less cost-consuming. This shift towards decentralized finance (DeFi) has been amplified with developments in permissionless, peer-to-peer platforms for how people and institutions access financial services. Web3 empowers smart contracts to support automated execution and allows tokenized investments in previously inaccessible assets restricted by location or wealth requirements. In this article, we will learn how the blockchain is disrupting the financial sector and discuss the increasing popularity of DeFi vs TradFi and the host of opportunities and obstacles that await.

Blockchain is a secure, decentralized digital ledger. Unlike the conventional financial system that relies on centralized entities like banks, the Federal Reserve, and clearinghouses to validate and process transactions, blockchains operate through a decentralized network of nodes. These nodes validate transactions using consensus mechanisms like Proof of Work or Proof of Stake, eliminating the need for centralized processing or entities. This model makes activity transparent, immutable, and resistant to unauthorized alterations making it fit for finance, supply chain, healthcare and more. It forms the backbone of DeFi protocols and holds the potential to revolutionize the financial world.

This innovation has given rise to digital currencies, tokenization of assets, and robust peer-to-peer payment platforms. By streamlining processes, blockchain reduces inefficiencies, minimizes costs, and accelerates transaction speeds. Traditional financial systems, with their multi-layered infrastructures and manual reconciliations, often face delays and high operational expenses compared to a decentralized money system. Blockchain addresses these challenges by embedding trust directly into its framework, confirming transactions are secure and tamper-proof.

The result is more accessible, efficient, and user-empowered financial institutions. Blockchain not only enhances productivity but also challenges conventional financial practices, paving the way for a future where technology drives transparency and cost-effectiveness in finance. The idea of central bank digital currency (CBDC) is emerging as a potential advancement that would mark one of the biggest changes in financial systems in decades. The Federal Reserve and other central banks are investigating CBDCs to potentially integrate TradFi with DeFi for improved financial accessibility and efficiency.

Decentralized finance (DeFi) is one of the most disruptive technologies of blockchain as it eliminates the need for traditional financial establishments. DeFi trading platforms allow traders to borrow, lend, and trade without an intermediary, but on smart contracts, which are programs that automatically execute on the blockchain.

On the other hand, TradFi includes traditional banking and institutionalized stock markets. Even though these establishments have been pillars of global economies for hundreds of years, they often receive backlash due to their exclusive nature.

Comparing DeFi vs TradFi reveals some key differences:

Access and Financial Inclusion: Anyone with internet access is able to use DeFi platforms, while TradFi often requires wealth minimums and specific locations, leading to unbanked and under-banked populations

Transparency: Blockchain systems are all record and maintain on distributed ledgers and therefore can easily be verified. In contrast, in TradFi, much is kept in the black box of a centralized entities private systems.

Costs: Through the use of DeFi, various services can be obtained at lower costs due to the absence of centralized intermediaries but in TradFi, hefty fees accompany banking services and asset management.

Centralized finance (CeFi) serves as a bridge between traditional financial systems and DeFi. CeFi relies on traditional financial theories while integrating cryptocurrencies, acting as an intermediary that offers users familiar services akin to banks. This facilitates financial transactions in both fiat and digital currencies, like PayPal combining cash and PYUSD in one wallet.

The tokenization of Real World Assets (RWA) is one of the most transformative use cases for blockchain innovations in the financial industry. RWA Tokenization converts tangible assets (such as real estate, precious metals, commodities and fine art) into a digital token asset on-chain. These digital assets can be traded, in lieu of the real asset, safely and easily into the financial ecosystem. Unlike normal ownership models, tokenized assets can be fractionalized to allow a much larger audience to buy in. These innovations are rapidly changing how we engage with traditional finance.

In the past, illiquid assets, such as real estate and luxury goods, were bought and sold with large currency and long periods of time. These assets are tokenized, which means they are divided into smaller units or tokens, such that investors can purchase fractional ownership. With the click of a button, investors can now easily acquire fractional ownership of high-value assets, such as luxury apartments, adding an entirely new level of liquidity in traditionally static markets.

Tokenization makes high-value asset investment less cumbersome. Traditionally, investing in premium real estate or art is prohibitively capital-heavy, restricting the asset class to rich individuals and institutions. With tokenization, anyone with a budget (modest) can now buy fractions of these digital assets, opening the way towards even greater participation in lucrative markets. The democratization of finance allows more people to participate and more people out of the economic system. And it closes the gap between individual investors and elite opportunities.

The basis for tokenization is blockchain technology, which offers a distributed ledger system that is immutable and secure. Ownership of assets can be accessed in real time so that there are no grey areas or conflicts. Also, the tokenized transactions do not require intermediaries, thereby lessening time, complications, and expenses associated with the traditional centralized exchanges. Further, the integration of blockchain into the transaction processes also increases the level of trust among investors since the provision of transaction history is complete and unchangeable.

Consider RWA tokenization in real estate. Companies no longer need brokers to divide the ownership of real estate. The art market was also transformed since artists could offer any fraction of their collections to the global market. The trading of commodities has also improved, enabling investors to conveniently purchase tokenized gold or oil.

All these mean that RWA tokenization is widening the opportunities in the financial market, and when coupled with the ease of trading cryptocurrencies, it will create an efficient ecosystem and new possibilities for investors. This comes as an encouragement for future investments and the promise of more effective mechanisms for the mobilization of capital.

Peer-to-peer payments enable money to move globally in a more streamlined manner; regardless of traditional intermediaries such as banks or payment processors, a user is able to move money to another directly using cryptocurrencies or stablecoins. In contrast, centralized exchanges act as intermediaries in Centralized Finance (CeFi), supporting both fiat and digital currencies.

This is a game changer for financial inclusion, especially in regions that are underserved or completely unbanked. Usually, this form of finance excludes millions due to geographical, infrastructural, or economic causes. Decentralized solutions seem to be the answer as they facilitate quick and inexpensive payments directly connecting the parties on a global scale.

Fintech, which refers to financial technology, is yet another way of disrupting the traditional financial systems, along with offering mobile banking and lending online, as well as digital wallets. With the help of blockchain technology, Fintech companies are able to broaden their scope of services through:

Decentralized Applications (dApps): Blockchain-based platforms relying on DeFi protocols create the possibility of providing services like lending, borrowing, and insurance with less dependence on third parties.

Digital Identity Solutions: Identity verification on the basis of blockchain guarantees security and ease of mounting customer registration on Fintech platforms.

Tokenized Financial Instruments: Another area of innovation is tokenization — made possible by blockchain — that makes by-Fintech firms appear more attractive to many investors by allowing the creation of entirely new investment products.

The integration of decentralized finance and Fintech has induced transformational creative growth never seen before, which calls for a future where services relevant to finance will be rendered in an efficient time period, cut across social gaps, providing equitable services for all. This future realizes a comprehensive financial ecosystem that allies traditional finance (TradFi) with decentralized finance (DeFi), boosting financial services accessibility, regulatory compliance, and consumer protection.

DeFi trading platforms are revolutionizing the finance industry as the central feature of blockchain. Users can trade cryptocurrencies, lending assets, or earn interest on liquidity pools – all within a transparent financial system that reduces risks from traditional parties.

DeFi trading platforms implement smart contracts, resulting in high levels of transactional certainty, reducing but not eliminating the likelihood of human errors or fraud, which differs greatly from deposits in the traditional finance systems.

As more of these platforms come into view, it begins to suggest there is a tendency for a more user-oriented structure of the financial industry, where a greater degree of control and involvement is expected. Nevertheless, these platforms are still subject to parameters of security and regulations to enhance their acceptance as mainstream methods compared to centralized financial services.

DeFi is not without its troubles, some of which include regulation, security, and scalability. Slow, central banks and the Federal Reserve still play a crucial role in stabilizing global financial systems and have responded to blockchain innovations with cautious interest, recognizing both its potential and the challenges it presents. Primary hurdles when it comes to use over traditional finance:

Regulatory Uncertainty: At the moment, governments and other authorities all over the globe are still trying to figure out the categorization and regulation of assets and systems based on blockchain technology. For instance, the U.S. SEC has been actively categorizing tokens as securities, sparking debates within the industry.

Scalability: For widespread usage and the ability to carry out numerous transactions, blockchain networks have to solve the scalability problem.

Security Concerns: Even if, in general, a blockchain is secure, exploits can occur owing to some vulnerabilities in the smart contracts or poor platform design. Unfamiliarity with the technology makes this concern even greater.

Integration with Legacy Systems: Introducing blockchain technology into the existing financial landscape is a challenge which necessitates investment and cooperation.

Oppositely though, the opportunities provided are as equally compelling. Further, blockchain enables:

Global Financial Inclusion: DeFi ensures adequate financial services reach the unbanked and under-banked populations.

Enhanced Transparency: Since it is impossible to alter or delete blockchain records, such technology guarantees reliability and responsibility when carrying out transactions.

Innovative Financial Products: Tokenized real estate, decentralized insurance, and other products illustrate how blockchain spurs imagination in developing financial stability.

It appears inevitable that the mixing of TradFi and DeFi will result in a hybrid financial system combining the best of both worlds. The traditional financial institutions are testing the use of blockchain technology to improve their offerings, while the DeFi ecosystem is coming up with ways to adhere to regulatory requirements and tackle scale issues.

This convergence, however, could make blockchain innovations such as RWA tokenization, peer–to–peer payments and decentralized lending seamlessly integrated into traditional finance and asset management.

The global financial crisis, such as the 2008 collapse of Lehman Brothers, significantly impacted the financial landscape and led to subsequent reforms aimed at preventing future crises. The decentralization, transparency, and efficiency of blockchain can overcome many inefficiencies of TradFi, thus making decentralized finance a serious competitor in redefining the financial industry. RWA tokenization, DeFi trading platforms and P2P payment solutions are already showing promise by creating faster, cheaper and more financially inclusive alternatives to the traditional systems. But TradFi is thoroughly embedded in the global economy supported by its regulatory frameworks, trusted institutions, and decades of infrastructural experience.

Instead, a hybrid model is probably what we can expect in the future whereby blockchain is supplemented by conventional finance. However, according to the report, the use of blockchain by TradFi institutions for settlement processes, digital asset management, and tokenization of financial instruments is becoming more common. At the same time, DeFi platforms are looking to overcome issues such as scalability and regulatory compliance to extend it to a broader mass audience. Herein lays the potential for this synergy to create a financial ecosystem in which blockchain facilitates TradFi with greater efficiency and inclusivity rather than displacing it wholesale.

Traditional finance is getting a makeover thanks to decentralization, which bolsters transparency, efficiency, and inclusivity. DeFi trading platforms, RWA tokenization and peer-to-peer payments aren't just challenging the status quo but creating a fairer, more open financial system. It’s only a matter of time until the DeFi and TradFi worlds collide, and the way the two interact will determine a future where financial services are truly democratized, pioneering, and agile.

Share this article

Related Articles

Related Articles

Related Articles